When you take a personal loan, most of the focus is on approval and disbursal. The money arrives, and the immediate need is solved. But the real experience begins after that. When it comes to repaying your loan, planning, discipline, and your understanding matter the most.

For urgent needs, options like FIRSTmoney personal loan by IDFC FIRST Bank provide disbursal up to ₹15 lakh in as little as 10 minutes. The 100% digital loan is available to individuals aged 21 to 60 with a stable monthly income and a CIBIL score of 710 or higher.

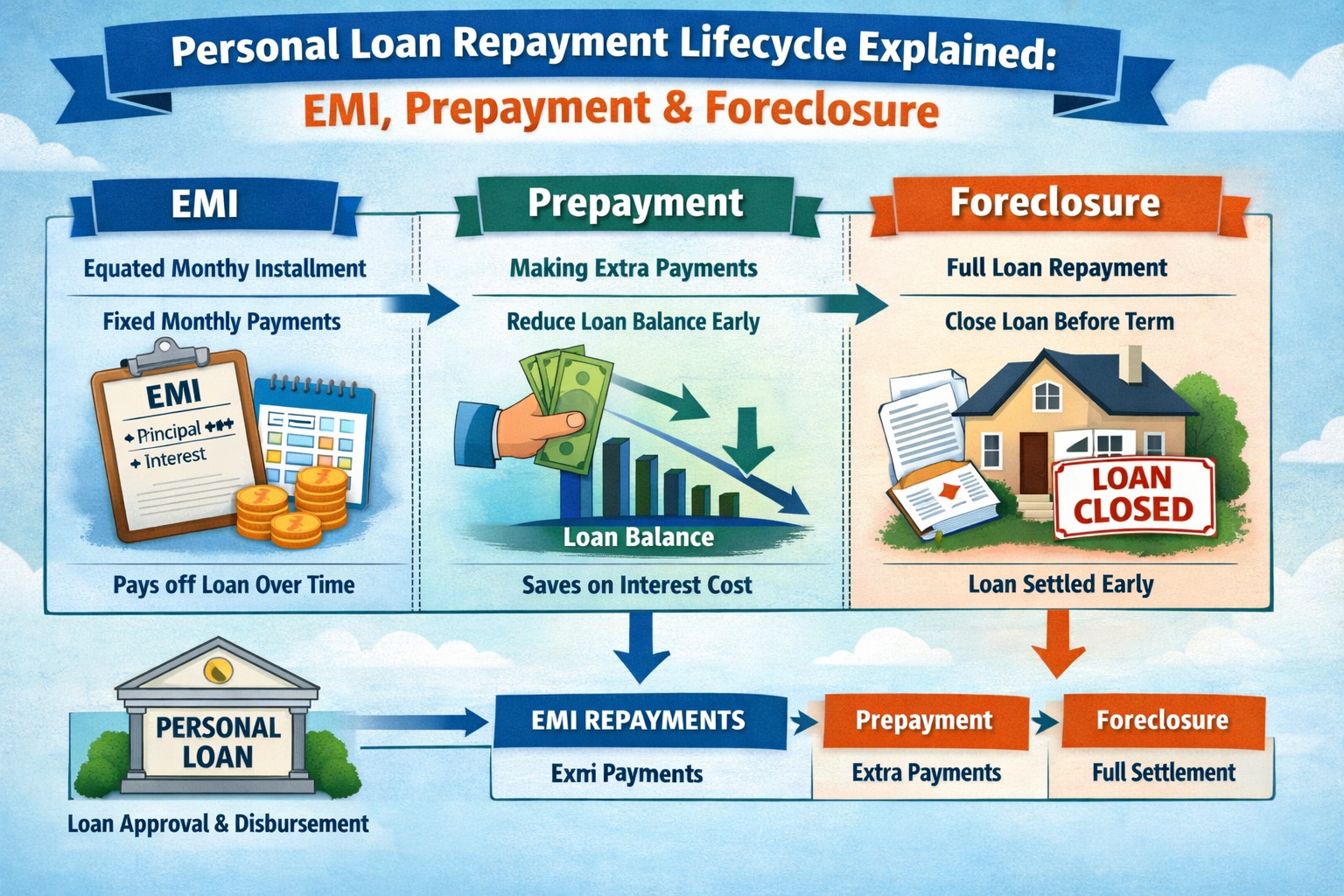

Understanding EMIs from the Start

The repayment journey usually begins with EMIs. An EMI includes both principal and interest. In the early months, the interest portion is higher. Over time, the principal portion increases.

Although this structure is normal, you might initially feel surprised when you see how slowly the balance reduces at first. So, when you know this in advance, it helps manage your expectations.

How Monthly Payments Shape the Loan

Your EMI stays consistent, but the impact changes over time. Each payment reduces your outstanding amount gradually. This reduction is what keeps the loan manageable.

If your income is stable, EMIs feel routine. If income fluctuates, they may feel restrictive. This is why understanding repayment structure matters before and during the loan.

Using Tools to Track Your Progress

An EMI calculator can help you understand how much interest you have already paid and how much remains via the amortization schedule.

In case of FIRSTmoney personal loan, all loan records, including repayment schedules, can be accessed through the IDFC FIRST Bank mobile app at any time. This digital access is part of a streamlined service for customers.

When Prepayment Becomes an Option

Prepayment means paying more than your scheduled EMI. This could be occasional or planned. Many borrowers choose to prepay when they receive bonuses or extra income. This prepayment can be in full or in part.

Prepayment reduces the outstanding principal. This, in turn, reduces future interest. Over time, this can shorten the loan tenure significantly.

For borrowers managing a personal loan, prepayment often feels empowering. It gives a sense of control and progress.

Thing to Check Before Prepaying

Not all loans allow free prepayment. Some lenders charge a prepayment fee. Others restrict the number of times you can prepay.

Understand these conditions before you go ahead and make extra payments. This will also help you avoid surprises and decide whether prepayment truly makes sense for you or not.

Foreclosure and What It Means

Foreclosure means closing the loan completely before the original tenure ends. Once foreclosed, no EMIs remain to be paid.

Many borrowers choose foreclosure when they have sufficient funds and want to be debt-free. However, foreclosure may come with charges, depending on the lender and loan terms.

You can consider options like FIRSTmoney Personal Loan by IDFC FIRST Bank where you don’t have to pay any foreclosure fees and can foreclose the loan easily via the lender app.

How Calculators Help with Prepayment and Foreclosure

Planning prepayment or foreclosure without numbers can be risky. This is where tools help again.

An EMI calculator online allows you to test different scenarios. You can see how prepayment affects tenure or total interest. This helps you decide the right timing and amount.

Why the Full Lifecycle Matters

Many borrowers focus only on getting the loan. But repayment defines the real cost and experience. Understanding EMIs, prepayment, and foreclosure gives you flexibility.

It allows you to adapt as your financial situation changes. It also helps you avoid stress when unexpected income or expenses arise.

Staying Disciplined Till the End

Consistency matters throughout the loan lifecycle. Paying EMIs on time protects your credit profile. Prepaying wisely reduces burden. Foreclosing at the right time gives closure.

Each stage has its value. When you understand them well, the loan works for you, not against you.

Final Thoughts

A personal loan is a journey that has multiple stages. Understanding the repayment lifecycle helps you feel prepared and confident.

You have choices available in each step – from EMIs to prepayment to foreclosure. When you make informed choices, you have high control and don’t need to stress about availing a personal loan.