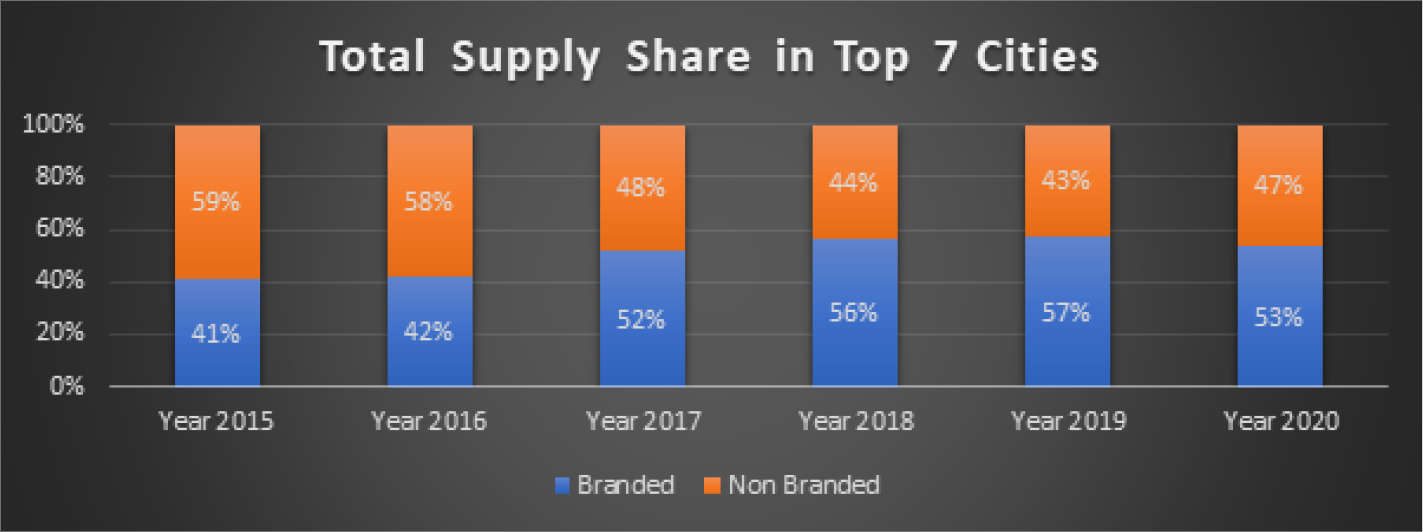

With consumer preferences tilting towards branded products over the last few years, the share of homes by branded players is on the rise across the top 7 cities. As per ANAROCK data, out of the total new housing supply in year 2015 (approx. 3.90 lakh units), branded players’ share accounted for 41% while the remaining 59% of housing supply was by non-branded players.

In 2020, the overall share by branded players has increased to 53% of the total supply (approx. 75,140 units in 2020 till September) across the top 7 cities. This clearly indicates that branded players have been increasing their supply to tap into the growing demand from homebuyers.

Another reason could be the liquidity crisis which the real estate sector has been grappling with over the last two years. Smaller players have had the short end of the stick – many of them face challenges with raising funds from banks and other financial institutions.

CITY-WISE TRENDS – 2020 VS 2015

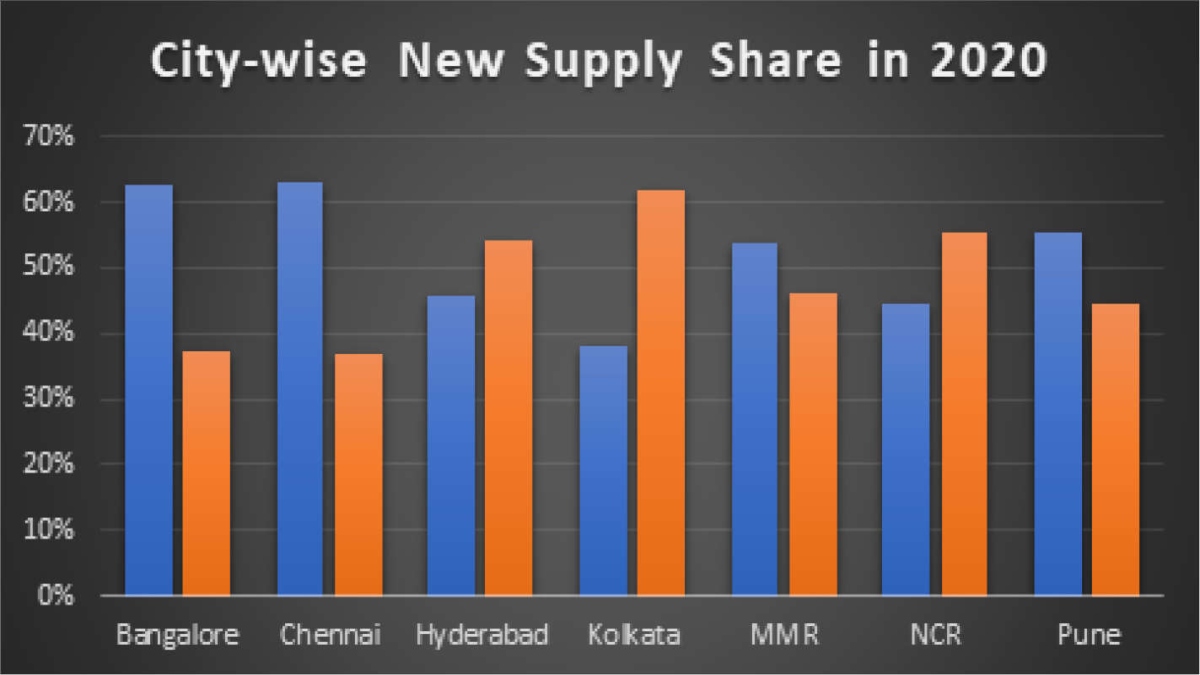

Of the total 15,020 units launched in Bengaluru in 2020 till September, a whopping 63% is by branded developers. In Chennai too, out of the total new launches of nearly 5,250 units in the city this year, branded developers share was 63%. In 2015, the ratio of branded vs non-branded players’ supply in Bengaluru stood at 52:48 and in Chennai it was 53:47.

In sharp contrast, new supply in Kolkata and NCR continue to be dominated by the non-branded players in 2020. Out of the total 13,000 units launched in NCR in 2020, nearly 45% is by branded players while 55% is by non-branded developers. Kolkata saw new supply of just 2,500 units in 2020 so far, of which 38% was by branded developers while a whopping 62% was by non-branded ones. Back in 2015, the ratio was 31:69 in Kolkata and 37:63 in NCR.

In MMR and Pune, the new supply share of branded developers in 2020 stands at 54% and 55% respectively. Back in 2015, the branded vs non branded ratio was 40:60 in MMR and 31:69 in Pune. Both markets have seen branded players’ share increase significantly over the years.

In Hyderabad, the new supply stood at nearly 8,300 units in 2020 of which the share of branded players is 46%. In 2015, the ratio of branded vs non-branded was the reverse – at 54:46.

2020 VS. 2019 TRENDS

Approx. 2.37 lakh housing units were launched across the top 7 cities in 2019, out of which nearly 57% (over 1.35 lakh units) were by branded developers and the remaining by non-branded players.

In 2020 (up to September), approx. 75,140 units have been launched, of which more than 53% are by branded developers. While the overall share in 2020 against 2019 declined marginally, the fact is that 2020 has seen a drastic reduction in the total number of overall housing units launched.

When the entire 2020 supply data becomes available by the end of December 2020, the share of branded players is very likely to have increased.

NOTABLE TRENDS BETWEEN 2019 VS 2020:

Despite consumer preferences generally skewed towards branded products, NCR saw the new supply share by branded players dip in 2020 from the previous year. In 2019, the ratio between branded and non-branded stood at 57:43 while in 2020 it stood at 45:55.

In Hyderabad also, new supply by branded developers saw a sudden dip in 2020 – from 61% share in 2019 the supply share fell to mere 38% in 2020. One reason could be that while branded players preferred to defer their new launches, non-branded players sought to launch projects that were previously approved and waiting to be launched.

Bangalore, Chennai, MMR and Pune, on the other hand, saw the new supply share by branded developers at almost same levels in 2020 as 2019.

(Note: ‘Branded’ developers include listed players, developers who have been operating for a decade and more, even newly-formed entities of large conglomerates and also those with sizeable areas under development either locally or Pan-India)

NCR & Kolkata new supply continues to be dominated by non-branded players in 2020 at 55% & 62% respectivel

Overall new supply share of branded developers jumped to 53% in 2020 against mere 41% in 2015 in top 7 cities altogether